ESG Rules May Be Narrower Now—But the Liability Standard Is Becoming More Audit-Grade

A surprising number of companies are misreading the EU’s sustainability rollback as relief.

What actually happened is more complicated—and potentially more dangerous.

The EU’s Omnibus I reforms materially narrowed the scope of the CSRD and CSDDD, raised thresholds, and pushed certain deadlines back. Many companies that expected to be in earlier reporting waves may now fall outside immediate mandatory filing requirements, while others have more time before the first report is due.

But the legal mistake is assuming that fewer mandatory reporters means lower liability.

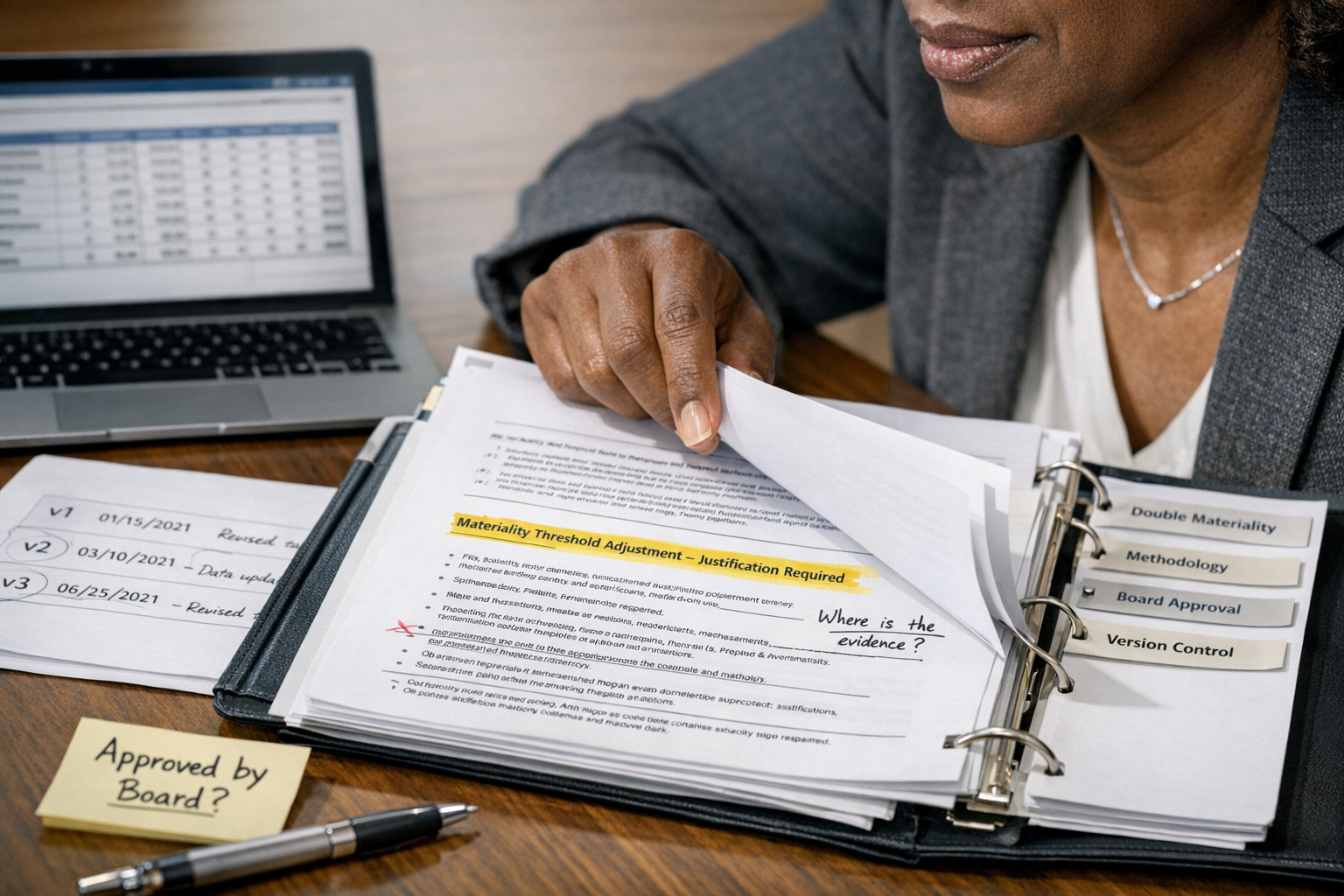

In reality, simplified rules do not mean simplified proof.

For the companies that remain in scope—or expect lender, investor, customer, or acquirer diligence around sustainability claims—the standard is becoming more audit-grade, not less. EFRAG’s updated technical direction preserves double materiality logic, versioned data methodologies, and legal evidence expectations even as datapoints are streamlined.

That shift is quietly increasing data risk.

Under the earlier framework, many leadership teams built ESG around volume: more datapoints, more disclosures, more templates, more teams collecting inputs. The Omnibus simplification changes the question. Now the real challenge is whether the reduced datapoints that remain can still be defended with a clear legal evidence trail, board-level signoff logic, and a version-controlled materiality methodology.

This is where many companies are unexpectedly more exposed.

A reduced reporting threshold does not eliminate the need to prove why certain topics were considered material, why others were deprioritized, what threshold changes were applied, and who approved the methodology shift. In practice, the simplification may actually make the decision logic itself more important than the raw disclosure volume.

That is why double materiality remains one of the most critical governance workflows.

Even where datapoints are reduced, companies still need to preserve how they evaluated financial materiality, impact materiality, stakeholder relevance, and board oversight over the changing thresholds. Recent EU guidance confirms that the distinct double materiality framework remains intact, albeit in a more streamlined form.

This is especially important for private companies that assume they are now “out of scope.”

They may still face:

lender ESG diligence

supply-chain disclosure requests

private equity diligence

regulated customer questionnaires

insurance underwriting

acquisition diligence

green-finance covenant testing

The legal issue is no longer simply whether the company files.

It is whether the company can prove how it made the ESG governance decisions it made.

That is where board controls are becoming the real pressure point.

When reporting thresholds change, the company needs a defensible record of:

what changed

when the threshold moved

which entity fell out of scope

which datapoints remained mandatory

what methodology was preserved

which board or committee approved the shift

what evidence supports the materiality conclusion

Without version control and governance traceability, simplification can actually increase litigation and diligence risk because the absence of prior disclosures raises more questions about the rationale behind the reduced dataset.

This is why the hidden liability in ESG simplification is not under-reporting alone.

It is unsupported governance logic.

The businesses that navigate this well are not celebrating smaller checklists. They are building stronger systems around reduced but still mandatory datapoints, preserving double-materiality workflows, maintaining legal evidence trails, tracking board signoff, and version-controlling threshold changes as the regulatory perimeter evolves.

That is exactly where the next generation of ESG compliance tools becomes valuable.

The future of ESG readiness is less about overwhelming reporting volume and more about defensible evidence architecture: clean workflows, documented board approvals, legal-grade audit trails, and threshold-aware version control when the rules change again.

For leadership teams navigating the post-Omnibus ESG landscape, this is the right time to review whether your current governance process can actually support reduced but still defensible reporting obligations. A focused legal and systems review often reveals where materiality logic, board signoff, evidence retention, and threshold versioning break down before diligence, investor scrutiny, or regulatory review turns “simplification” into an avoidable liability event. If your team is reassessing ESG obligations after the EU rollback, this is the ideal moment to schedule an ESG governance consultation and get early access to TEIL’s ESG compliance platform—built to preserve evidence trails, double-materiality workflows, and board-ready version control as the rules continue to evolve.